Ethical Investing

At Wealthify, we know how important it is to be able to invest in line with your values.

It’s why we’re proud to offer five different Ethical Investing Plans that:

- Favour best-in-class fund providers from an ethical standpoint.

- Invest in funds that aim to exclude tobacco, gambling, controversial weapons, and adult entertainment.

- Keep fees low with a simple annual management fee.

Investing gives your money the opportunity to grow over the long term, although returns can rise and fall with market conditions. Tax on your investment depends on your individual circumstances and can change.

How to open an ethical investing account

Start your ethical investing journey with Wealthify in three simple steps:

Step 1

Choose your investment product, style, and how much you want to invest.

Step 2

Complete our investment suitability quiz.

Step 3

We build and manage your Ethical Plan for you!

Awards

Our ethical investment accounts

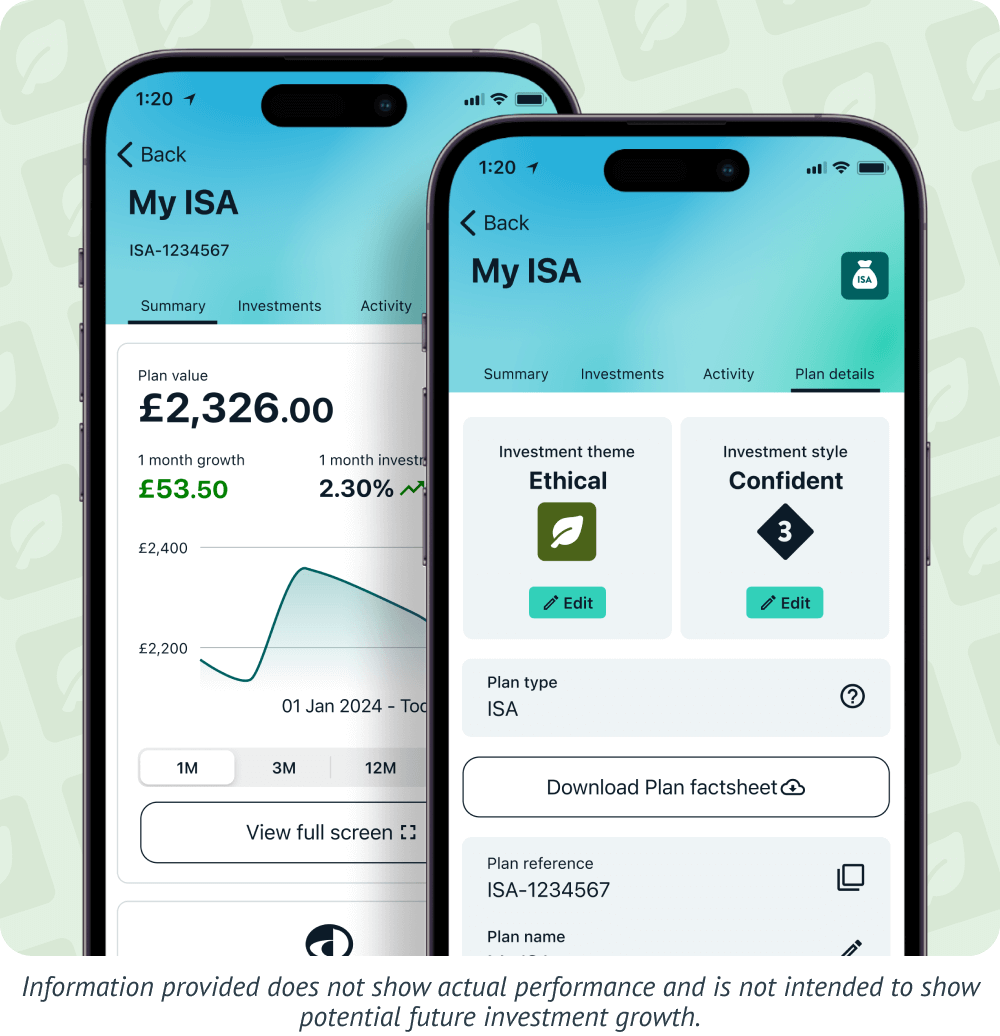

Investment ISA

- Invest up to £20,000 each year with no capital gains tax or income tax.

- Pay withdrawn money back in the same tax year — without affecting your annual allowance.

- Withdraw your money at any time, without penalty.

SIPP

- Combine previous pensions into one handy pot, making it easy to track and manage.

- Automatic 25% top-up when you make further contributions.

- Reduced fees on balances over £100,000.

JISA

- Invest up to £9,000 every year for each child without paying tax on growth.

- Family and friends can contribute directly too.

- Easily transfer another Junior Cash ISA or Child Trust Fund to your Wealthify Junior ISA.

GIA

- Invest as much as you like with no upper limit and low management fees.

- Access the same expertly managed investment Plans as our Stocks & Shares ISA.

- Withdraw your money at any time, without penalty.

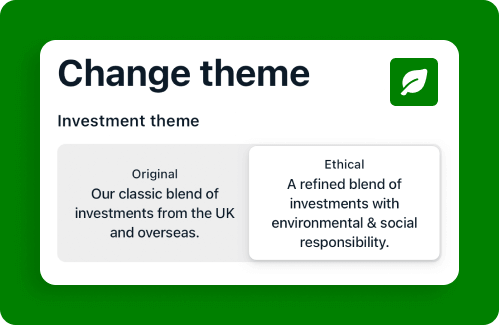

What is ethical investing?

Defining an ethical investment is subjective, with one investor's exclusion being another's essential holding.

At Wealthify, our Ethical Investing Plans contain funds that go further in their objective to deliver positive ESG (Environmental, Social, and Governance) outcomes.

These funds focus on social and environmental goals, with some seeking alignment with targets such as the Paris Agreement.

As part of our ongoing commitment to maintaining these standards, our Investment Team regularly review whether the funds we use continue to select best-in-class companies and maintain their ethical screening standards. The fund providers we use have a 10% (maximum) tolerance when they screen for tobacco, gambling, controversial weapons, and adult entertainment.

If those standards change (i.e. a fund is downgraded in its sustainability classification or a manager softens its commitments), we might conduct a review to consider alternative funds.

How do we pick what ethical funds to invest in?

In simple terms, we don't just select the least harmful funds, but the ones actively directing their money and efforts towards meaningful, measurable solutions.

By choosing best-in-class ethical investing funds, our Ethical Investing Plans reward industry-leading companies, pressuring those falling behind to improve their efforts. All our fund providers are signatories of the Principles of Responsible Investing (PRI), the world’s leading proponent of responsible investing.

We believe companies driving positive engagement drive more meaningful change than blanket exclusion, with the latter penalising those making genuine progress. Likewise, over-restrictive screening can potentially reduce diversification and undermine long-term returns.

Our selection is determined by three levels of sustainability commitment. As a result, funds must:

Apply sustainability screening and best-in-class selection

Favouring companies with stronger ethical and sustainability credentials within each sector.

Showcase dedicated sustainability objectives

Targeting specific positive outcomes, such as climate transition or Paris Agreement alignment.

Be open about how they invest responsibly

Providing evidence of their sustainability commitments, including published stewardship policies, ESG reporting, and active ownership practices.

Other need-to-knows

It’s also important to understand the role oil and energy companies – as well as government bonds – play.

Government bonds form an essential part of our Ethical Plans’ performance and stability.

Although government bonds don't adhere to the same sustainability classification framework as corporate investments, we favour ones from developed, democratic nations with commitments to international climate agreements.

Some funds we choose may hold positions in oil, gas, or integrated energy companies.

This is a deliberate aspect of our approach, as ethical investing doesn’t always mean a blanket exclusion of the energy sector.

Instead, we look for funds which include energy companies with credible transition plans and verified science-based targets, while excluding the most harmful activities such as thermal coal extraction, tar sands, and controversial drilling.

Why choose Wealthify?

As well as providing best-in-class funds, here's how we've made it really simple to start ethical investing with confidence:

✓ We keep fees low, with a simple annual management fee of 0.6% p.a., and fund and trading fees of approximately 0.58% p.a. for Ethical Plans.

✓ You can change your investment style at any time, with no extra cost.

✓ Easy-to-use investment app and dashboard to track your Plan(s) performance.

✓ Our award-winning, human Customer Care Team is on hand to help.

✓ We’re owned by Aviva, one of the UK's largest financial institutions.

How have Wealthify Investment Plans performed?

The graph below shows how each of our investment styles - from Cautious to Adventurous - have performed between 29th February 2016 and 30th April 2026, after all fees have been taken (based on 0.60% p.a. Wealthify management fee). These figures are based on the performance of Plans worth more than £100, figures will be different for Plans below that amount.

Original

Ethical

Of course, we experienced the ups and downs of the market along the way and you could get back less than you put in. Although we cannot rely on past performance to predict future results investing for the long-term (5 years or more) typically delivers positive returns. These figures are after all fees have been taken (based on 0.60% p.a Wealthify management charge), and are based on the performance of Plans worth more than £100 and will be different for Plans below that amount.

Plan performance by year

This table shows by how much each of our investment styles have grown each year

| Investment Style | 31/12/2020 - 31/12/2021 | 31/12/2021 - 31/12/2022 | 30/12/2022 - 30/12/2023 | 29/12/2023 - 29/12/2024 | 30/12/2024 - 30/12/2025 | 30/04/2025 - 30/04/2026 |

|---|---|---|---|---|---|---|

| Cautious | 0.56% | -11.06% | 4.72% | 1.31% | 6.16% | 4.95% |

| Tentative | 3.85% | -10.53% | 6.37% | 3.48% | 8.34% | 9.94% |

| Confident | 6.81% | -9.91% | 7.99% | 6.29% | 10.38% | 15.15% |

| Ambitious | 9.83% | -8.89% | 9.71% | 9.35% | 12.24% | 20.09% |

| Adventurous | 12.91% | -9.18% | 11.61% | 12.56% | 13.81% | 25.10% |

How have Wealthify Investment Plans performed?

The graph below shows how each of our investment styles - from Cautious to Adventurous - have performed between 13th August 2018 and 30th April 2026, after all fees have been taken (based on 0.60% p.a. Wealthify management fee). These figures are based on the performance of Plans worth more than £100, figures will be different for Plans below that amount.

Original

Ethical

Of course, we experienced the ups and downs of the market along the way and you could get back less than you put in. Although we cannot rely on past performance to predict future results investing for the long-term (5 years or more) typically delivers positive returns. These figures are after all fees have been taken (based on 0.60% p.a Wealthify management charge), and are based on the performance of Plans worth more than £100 and will be different for Plans below that amount.

Plan performance by year

This table shows by how much each of our investment styles have grown each year

| Investment Style | 31/12/2020 - 31/12/2021 | 31/12/2021 - 31/12/2022 | 30/12/2022 - 30/12/2023 | 29/12/2023 - 29/12/2024 | 30/12/2024 - 30/12/2025 | 30/04/2025 - 30/04/2026 |

|---|---|---|---|---|---|---|

| Cautious | 0.80% | -14.80% | 4.80% | 0.60% | 5.30% | 4.20% |

| Tentative | 4.10% | -15.20% | 6.90% | 2.90% | 5.80% | 8.40% |

| Confident | 7.70% | -15.70% | 8.90% | 5.30% | 6.30% | 12.50% |

| Ambitious | 11.10% | -16.30% | 11.10% | 7.60% | 6.50% | 15.90% |

| Adventurous | 14.50% | -17.60% | 13.30% | 10.30% | 6.40% | 19.60% |

Ethical guide

If you want to learn more about ethical investing and its significance, we've created a comprehensive guide to help you explore how it works, ways to invest ethically, key considerations, and much more.

This guide doesn't offer personal advice, speak to a financial adviser if you're unsure about whether investing is right for you.

Wealthify Customer Reviews

Ethical Investing FAQs

Environmental, Social and Governance (ESG) aims to actively identify companies to invest in that demonstrate excellent environmental, social and governance practices. Fund managers might look at a wide range of factors: how much energy a company wastes; its overall impact on the environment; what it does to champion gender and race equality; whether it gives back to its communities; whether suppliers hold similar values; how transparent it is in reporting and whether its shareholders can vote on important issues. A complex scoring system is often used to determine a company’s ESG score, which determines whether it is a suitable investment. ESG fund providers constantly monitor and review the companies they invest in using these criteria to ensure standards remain in line with the aims of the fund.

Sustainable Investing: aims to generate positive social outcomes. It’s typically a blend of ethical investing (excluding companies involved in ‘harmful’ activities) and ESG investing (identifying companies that demonstrate good behaviour). This blend of negative and positive screening aims to capture the best of both worlds and, some argue, is a more ethically sound approach.

Impact Investing: aims to achieve specific benefits, whether social or environmental, as a result of the investment, as well as a positive return. It’s generally considered as a subset of sustainable investing, but does not necessarily aim to exclude activities which can cause harm. Impact investing seeks to make a positive impact by investing, for example, in enterprises that benefit the community, or in clean technology. It might also invest in companies involved in harmful activities if they can demonstrate they are taking action to significantly reduce their reliance on it to generate profit, or even switch to more sustainable activities.

We’re using best-in-class ethical fund providers: Edentree, Pictet, Liontrust, Royal London, Stewart Investors, Brown Advisory, and Rathbone. They have been selected for their exemplary quality of governance and ethical stance, and each employ rigorous and ongoing screening processes to ensure appropriate ethical credentials for the relevant funds.

All of the ethical fund providers we use are signatories of the Principles of Responsible Investing (PRI), the world’s leading proponent of responsible investing. The PRI is an independent body acting in the long-term interests of its signatories, of the financial markets and economies in which they operate and ultimately of the environment and society as a whole. More information: about the PRI.

We use a pool of up to 25 funds to build your Ethical Plan. The combination of funds we use depends on your investment style and how we balance your Plan. The pool of funds will also change from time to time.

We use a blend of active and passive ethical funds in our Plans. Active funds get their name because they are ‘actively’ managed. We think this is a robust way to manage our Ethical Investment Plans, as active ethical funds can take a far more qualitative approach, using a wider set of criteria — and applying a common-sense approach to selecting sustainable investments.

Passive funds, on the other hand, use a fixed Environmental, Social, and Governance (ESG) score to screen companies, offering little flexibility. Passively-managed ethical funds are also unable to exert shareholder pressure on individual companies to drive positive change.

Current list of funds:

- M&G European Sustain Paris Aligned Fund

- EdenTree Responsible and Sustainable Short Dated Bond Fund

- iShares UK Gilts All Stocks Index Fund

- Liontrust Sustainable Future UK Growth Fund

- Liontrust Sustainable Future Global Growth

- Liontrust Sustainable Future European Growth

- Rathbone Ethical Bond Fund

- Royal London Ethical Bond Fund

- Royal London Short Duration Gilt Fund

- Royal London Sustainable Leaders Trust

- Stewart Investors Asia Pacific Sustainability Fund

- Stewart Investors Global Emerging Markets Sustainability Fund

- Stewart Investors Worldwide Sustainability Fund

- Royal London Short Term Money Market Fund

- JPM Emerging Markets Sustainable Fund

- Fidelity UK Gilt Fund

- Brown Advisory US Sustainable Growth Fund

- FTGF ClearBridge US Equity Sustainability Leaders Fund

- Fidelity Funds - Sustainable Japan Equity Fund

- Pictet - Global Environmental Opportunities

- Vanguard U.S. Government Bond Index Fund

- Vanguard Euro Government Bond Index

Please note: the funds and fund providers we use will be reviewed and may change from time to time, which may not immediately be reflected here.

Funds 17 to 22 are based overseas and are not subject to UK sustainable investment labelling and disclosure requirements.

For more information, please see: https://www.fca.org.uk/consumers/sustainable-investment-labels-greenwashing

Our Ethical Plans are built using mutual funds. The funds contain multiple investments, selected by the fund providers according to their strict ethical screening processes.

The funds will typically include:

Shares (owning a piece of a company): excluding companies that profit from ‘sin sectors’ such as gambling, tobacco, adult entertainment and weapons among others. It will only include companies that demonstrate great environmental, social and governance standards, according to the fund providers’ and Wealthify’s strict criteria and ethical investing policies.

Bonds (an IOU from a government or company with some interest): both corporate and government bonds may be included and will be subject to the same strict screening criteria as shares.

Thematic investments: one or two funds will focus on investing themes such as gender equality (companies that strongly champion these issues) or green energy and will mostly be used in higher risk plans.

We’ve created five Ethical Investment Plans – from Cautious to Adventurous – so you can choose a level of risk that’s right for you. Find out more about what’s in each of these plans by downloading the ethical plan factsheets, below.

Ethical Plan Factsheets

Cautious Ethical Plan [download pdf]

Tentative Ethical Plan [download pdf]

Confident Ethical Plan [download pdf]

Ambitious Ethical Plan [download pdf]

Adventurous Ethical Plan [download pdf]

Fund providers will typically exercise two levels of screening:

Negative screening: aiming to exclude companies involved in activities that are at odds with ethical and socially responsible values. This typically means ‘sin stocks’ such as gambling, tobacco, adult entertainment and weapons, although most funds screen many more activities besides.

Positive screening: actively seeking and investing in companies that demonstrate excellent environmental, social and governance (ESG) practices. More about what this means can be found in What is ESG, sustainable and Impact investing? Fund providers will employ a scoring system to each company, rating it against a set of predefined criteria, such as energy efficiency, equality agenda and the quality of its corporate governance, looking at, for example, whether it has been fined in the past for regulatory violations. These all add up to an ESG rating, which determines whether a company should be considered for investment. Our ethical funds don’t just invest in companies with the highest ESG ratings. They will also identify and invest in ‘improving companies’ – i.e. those that show significant commitment to improving their environmental, social and governance practices. An example might be a coal company that is investing a significant part of its profits in the research and development of green energy.

Ethical fund managers with 'actively managed' ethical funds will regularly search for new companies to invest in, whilst also monitoring the activities and practises of the companies already in the fund to ensure that the expected standards are maintained.

As shareholders, funds can even use their influence and voting power to steer the organisation towards ever higher ethical standards, attending AGMs and lobbying the board of directors. Where the fund holds a significant shareholding (e.g. 10% or more) they may get an audience with the board of directors where they can highlight issues and help influence the strategic direction of the organisation. Ethical fund providers sometimes join forces to wield more influence over the board, if their own shareholding is too small.

If a company consistently allows its standards, and therefore its ESG rating, to slip, fund managers are able to withdraw investors’ money and remove the company from the fund.

All ethical fund providers with 'actively managed' ethical funds have built a level of independent verification into their processes — usually carried out by an autonomous and impartial organisation — to ensure that no bias creeps into the fund’s screening and monitoring process.

Wealthify also has its own code of practice, set out in our ethical investing policy. Our investment team will regularly monitor the ethical funds using specialist ESG company assessments conducted by a third party, to ensure that their standards of practice are not falling below what is expected.

Each fund provider will negatively screen (i.e. exclude) companies involved in certain sectors and activities. Typically, these will be ‘sin sectors’ such as gambling, tobacco, adult entertainment and weapons. The full list of sectors considered can be much wider.

The exclusion criteria also vary between providers: some funds will completely exclude a company profiting from harmful activities (e.g. tobacco) whilst others may invest in the company, provided it earns no more than 10% of its overall profits from the activity in question. This 10% tolerance allows a small degree of flexibility to account for instances where a company isn’t directly involved, but could be exposed to a harmful activity via, for example, a parent company or supplier. Fund managers argue that earnings of less than 10% demonstrates there’s effectively no significant involvement in that activity and an investment in the company is justifiable.

A 10% tolerance is applied to the screening of some activities by the fund providers we use. Therefore, we can never guarantee that our plans will not contain some degree of exposure to any of the harmful activities listed.

Our ethical funds aim to exclude the following, subject to an up to 10% tolerance: tobacco; gambling; controversial weapons; and adult entertainment.

Returns are not guaranteed with any form of investing and you could get back less than you put in.

With all types of investing, cost affects your performance, as the more you pay in fees and charges, the fewer returns you get to keep. The overall cost of investing in an ethical plan is higher than that of a standard plan and therefore, investing in an ethical plan may affect performance and your returns could be lower than a standard investment plan with an equivalent investment style. Ethical funds aim to avoid investing in certain sectors, like tobacco or gambling, which could also affect your plan performance.

You can get some idea of how ethical investments perform against their standard counterparts by comparing market indices like the FTSE for Good against the FTSE All Share. Of course, past performance is not a reliable indicator of future performance.

We use a blend of active and passive funds in our ethical plans, so the average fund charge is a little higher than in standard plans. Check our fees page for the most up to date ethical fund charges and transaction costs. The extra cost of active funds reflects the fact that they are proactively and comprehensively managed using a qualitative and common-sense approach to select the most appropriate investments and to ensure standards are retained. We think this makes for a more robust ethical investment plan.

The annual cost of investing will depend on how much you invest and which investment style you choose. The total cost of investing is comprised of your annual management fee which covers everything we do, plus fund charges and transaction costs. Check out our fees page for full details.

We do have fewer types of investments at our disposal to create Ethical Plans, but we still use the main two types of investment – shares and bonds – as well as some thematic investments, for a bit of variety. Your plan will also hold a small amount of cash, which is common practise to enable our team to be flexible in buying investments on your behalf.

If you already invest with us, you’ll need to get in touch with our customer support team who can assist you further. Call 0800 802 1800, or send us a secure message via your Wealthify account by clicking the 'Messages' link.

At Wealthify, we invest in ethical funds which pro-actively select companies that are committed to having a positive impact on the environment and society. But it doesn’t stop there! In addition to selecting the different funds, our investment team actively monitor the companies that are being selected by fund managers.