People often think that investing is a complex, intimidating and expensive process that requires a wealth of knowledge and a substantial amount of money to get started.

Investing might seem scary initially, especially since there are so many myths surrounding it. However, the process isn’t as daunting as it appears — and making decisions based on fear could be stopping you from securing your financial future.

We surveyed 2,000 people from the British public that have £5,000+ in savings but haven’t invested before1, looking to uncover the main reasons why people don’t invest — and to help clarify the numerous misconceptions surrounding investing.

The research reveals that preference to put money in a savings account was one of the main investment barriers, with 85% of Brits sharing this belief.

The findings show that 52% of people haven’t even considered investing in the past year, with older age groups being the least likely to invest their money. Just 20% of those aged 66+ have considered investing in the past year. In comparison, 68% of Gen-Z have considered investing, showing a clear generational divide when it comes to investing.

The main barriers to investing

The top barrier to investing was preference to save in a cash account, followed by a fear of getting scammed. Seventy percent agree that a perceived lack of knowledge is a main reason for not investing, with a further 69% saying they don’t trust where their money will be going.

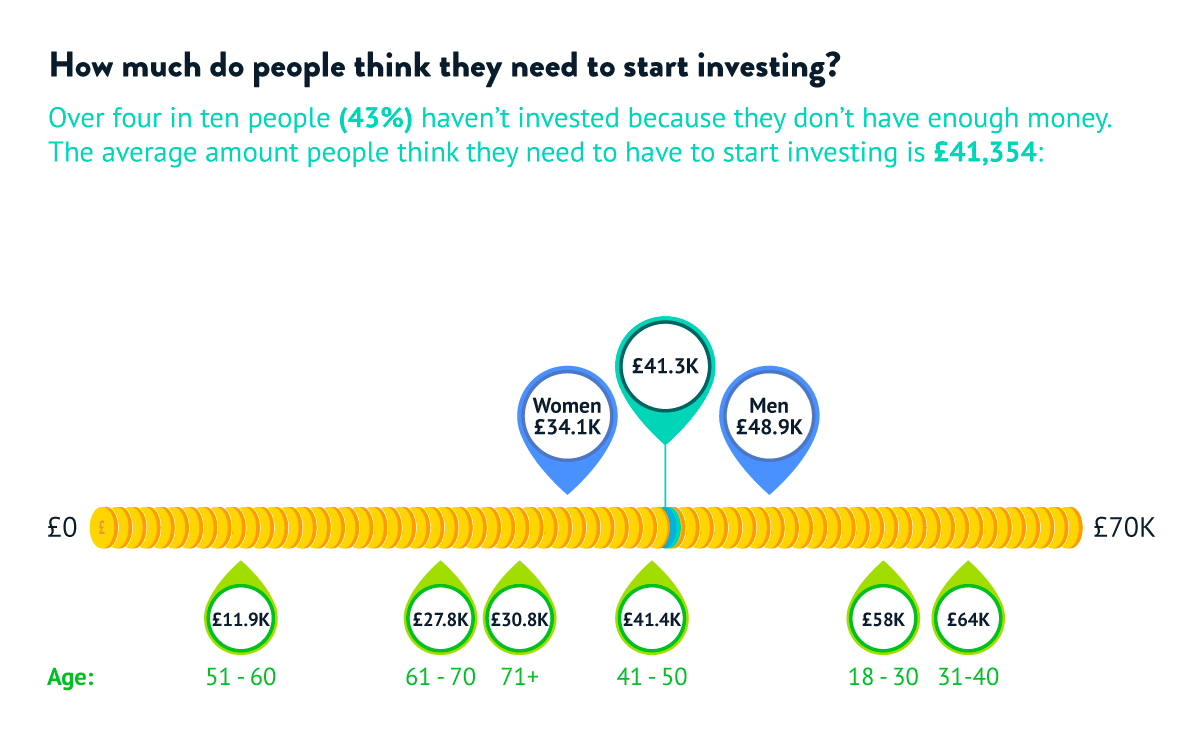

A common investing misconception is that people think they need to start with a huge amount; in fact, over four in ten people (43%) haven’t invested because they don’t have enough money. According to our research1, the average amount people think they need to have to start investing is £41,354. However, in reality, you can start with a lot less.

Our study also found that many people have been putting off investing due to feelings of nervousness; two thirds (66%) said they haven’t invested because the thought of it makes them nervous, with some having a fear of making a mistake or losing money. For many of these people, having experts manage their money can help alleviate these concerns and make the prospect of investing less daunting.

However, one thing to keep in mind is that with all types of investing, your capital is at risk. This means that the value of your investments can go down as well as up, and could get back less than you initially invested.

For more information, check out our Stocks and Shares ISA page.

Is your money better off in a savings account?

A large percentage of people (85%) haven’t invested because they’d like to put their money in a savings account; the main reasons for this being, needing quick access to their money (95%) and less risk of losing it (94%). However, this might not be the best or safest option, experts say.

Andy Russell, CEO at Wealthify: “There’s no denying that savings rates are particularly attractive at present. However, when we look at the rate of inflation – which is still in the double digits despite expectations it would fall below 10% in April – there is still a big gap between that and the interest rates on cash accounts. So, if the interest rate on your cash savings is below inflation, that means over time your money will lose value.

“So, if the interest rate on your cash savings is below the level of inflation – which is extremely likely – over the long term, your money will lose value, as you’ll be able to buy less with it. That leaves us with the question, what’s the real risk – investing your money for the long term, or leaving it in a cash account to be eaten away over time?”

In the study, we presented participants with a chart that shows the returns generated by investing in the FTSE 100 versus placing the same amount of money in a savings account over a 10-year period (2012-2022).

Over half (52%) of people agree that after seeing how an investment may have grown over the past 10 years, they feel more confident about investing their money. However, one thing to keep in mind is that past performance is not a reliable indicator of future results, and this doesn’t include investment fees they would have paid.

The challenges women face in the investment landscape

Our study also unearthed some stark differences in the attitudes towards investing between men and women. A staggering 73% of women don’t feel confident investing their money — compared to just 58% of men. And the same goes when it comes to knowledge: 73% of women haven’t invested because they don’t think they are knowledgeable enough, versus 67% of men.

Despite women being more likely to have financial goals than men – with 61% of women saying they have definite savings goals for the future, compared to 49% of men – our research found that many are hesitant about investing their money.

The study shows that 87% of women have chosen to put their money in a savings account rather than investments, with more than one in four (26%) women believing investing is not an option for them.

Interestingly, the majority of women (90%) say they’d be more likely to invest if they were more knowledgeable about it; another 89% said they’d be more likely if there was a clear route as to how to do it. And over three quarters (77%) of women say they’d be more likely to invest if they had access to a financial planner/advisor.

Aligning investing with making a positive impact is also something that might make more women consider investing. Over seven in ten women (73%) state they’d be more willing to invest if they felt the funds or investment vehicle were supporting good causes.

Michelle Pearce, Co-Founder at Wealthify: “Confidence and lack of knowledge remain key barriers stopping women from investing, despite the many digital investment services – like Wealthify – that aim to remove the jargon from investing and make it as accessible and understandable as possible.

“You don't have to be a financial expert to start. In fact, you don’t need to know anything if you don’t want to. Just trust the experts to take care of it for you. And if you’re unsure, you can start small and build your way up.

“Our belief is that everyone deserves the chance to invest and ensure their financial stability. And, as such, we want to encourage women to take charge of their financial future.”

Top regions where people are most likely to invest in the future

Our research also sought to explore regional differences when it came to the likelihood of investing. Interestingly, Londoners are most likely to invest in the future, with 64% saying so, followed by Northern Ireland, where 58% of people shared a similar sentiment.

In comparison, just 36% of people in Scotland said they are likely to invest in the future, making it the region least likely to invest. Following closely behind is Yorkshire, with only 39% of people saying they are likely to do so.

Investing for Gen Z: younger generations take the lead

Younger people seem to be more interested in investing, compared to older generations.

Over two-thirds (68%) of 18 to 25-year-olds have considered investing in the past year, which is more than the general public — of which only 48% have considered it.

Even though Gen Z is more likely to invest compared to any other generation, there are still barriers for them. Six in ten 18 to 25-year-olds (62%) haven’t invested because they think it’s too time-consuming. And 61% haven’t invested because they’re worried they won’t be able to access their money.

Interestingly, over half (54%) of Gen Z (18-25) haven’t invested because they believe their money would be supporting causes that don’t align with their own values (compared to this being a barrier for 37% of the rest of the nation.)

The sooner you start, the more potential your money has to grow, so it’s worth considering joining the investment world as soon as you are able to.

Andy Russell, CEO at Wealthify comments: “We live in a digital era that allows us to start investing with just a few clicks — meaning it’s now accessible to pretty much anyone.

“With online investment products that are available now like Investment ISA, you don’t necessarily need expert investment knowledge or a ton of previous experience to start. And for those concerned with investing in line with their values, there are lots of ethical options out there.”

Please remember the value of your investments can go down as well as up, and you could get back less than invested.

Wealthify does not provide financial advice. Seek financial advice if you are unsure about investing.

1Research conducted on behalf of Wealthify by Savanta amongst 2,000 UK adults that have £5,000+ in savings and have not invested before in March 2023.

|